As an informed investor, you are likely familiar with the standard financial advice: "Keep three to six months of expenses in a savings account". However, when optimizing your wealth, you quickly recognize the inherent friction in this rule. Holding tens of thousands of dollars or euros in a low-yield asset introduces a severe cash drag on your portfolio, strictly limiting your long-term compounding potential.

Instead of viewing your emergency fund as a stagnant pool of cash, you should treat it as a dynamic, 3-tiered liquidity strategy. This article breaks down the strategic mechanics of optimizing your household liquidity, balancing the safety of cash against the opportunity cost of lost investment growth.

1. What is a Strategic Emergency Fund and Why Do We Need One?

At the professional wealth management level, household reserves are guided by the macroeconomic "buffer-stock theory" (Caroll, 1992 and Caroll, 2021) of saving. This model demonstrates that households optimize their financial stability by balancing their natural impatience for consumption with a prudent need to insulate themselves against unpredictable income fluctuations. This underlying economic principle applies universally, driving precautionary saving behaviors during economic downturns across both the US and Europe.

To optimize your buffer, we must stop treating all emergencies as identical events. Personal financial shocks generally fall into two distinct risk categories:

-

Spending Shocks: These are unwanted, unplanned, and highly probable expenses, such as a major home repair or an unexpected out-of-pocket medical bill. Because these events are a semifrequent and virtually inevitable fact of life, they demand a strategy of absolute capital preservation. You buffer against spending shocks using quick assets - such as highly liquid cash equivalents in checking accounts or money market funds - ensuring you have immediate access to funds without being forced to sell investments at a loss.

-

Income Shocks: Income shocks involve an unexpected loss or reduction of employment income, such as a sudden layoff or a drop in wages. Unlike spending shocks, income shocks are generally rare, and some households may never experience one. However, their financial consequences are significantly more severe. The primary danger of an income shock is that it can force you to liquidate long-term investments during a market downturn to cover your living expenses, severely compounding your financial losses. Because they are infrequent, income shocks do not require holding massive amounts of uninvested cash. These are deeper reserves invested for long-term growth (such as Roth IRAs, Health Savings Accounts, or taxable brokerage accounts) that are mathematically "overfunded" to survive potential market drawdowns while remaining accessible

An optimized emergency fund addresses both shocks with different asset classes, matching the accessibility of the capital to the specific probability and severity of the event.

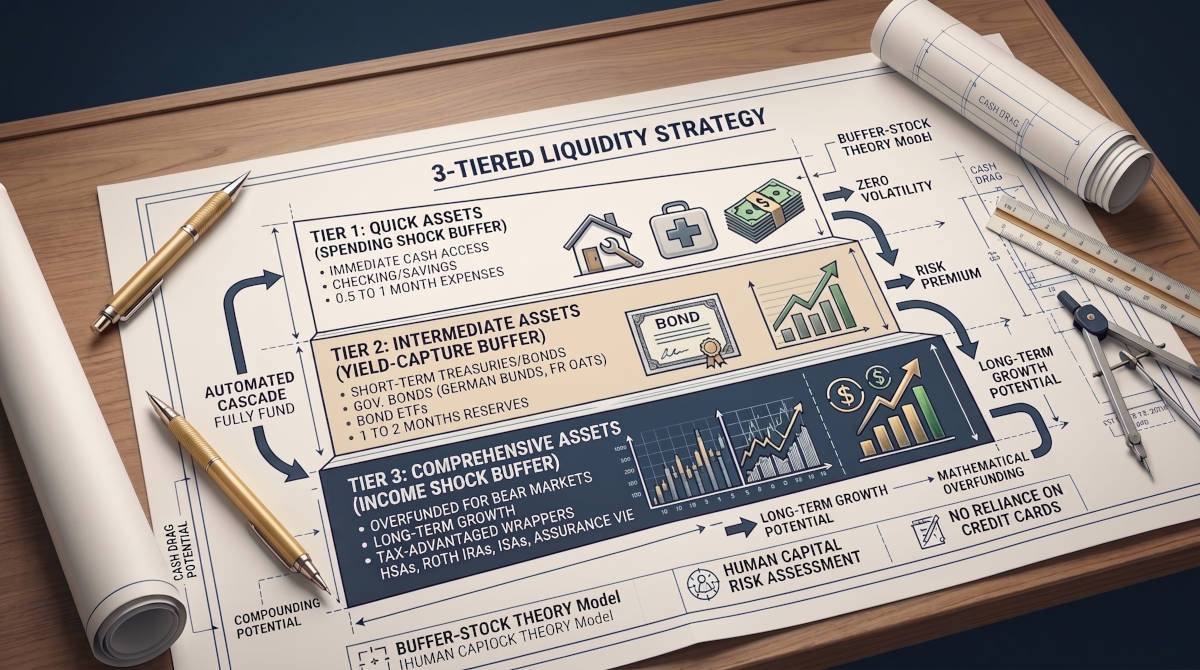

2. The Basic Structure: The 3-Tiered Liquidity Blueprint

Classical financial models demonstrate that household emergency reserves are best categorized into three layers: quick, intermediate, and comprehensive assets. By adopting this 3-tier structure, you bridge the gap between absolute capital preservation and long-term yield generation.

Tier 1: Quick Assets (The Spending Shock Buffer)

- The Strategy: You need immediate, penalty-free access to cash for inevitable spending shocks. This money must be accessible in a day, but not instantly, shielding it entirely from stock or bond market volatility so you are never forced to sell equities at a loss to fix a leaky roof.

- US vs. EU Execution: Hold up to 1 month of living expenses in a highly liquid checking account, everyday savings account, or money market fund.

- Note on the EU context: Because most EU nations feature robust universal healthcare systems, the risk of a catastrophic out-of-pocket medical bill is significantly lower. Therefore, an EU investor's Tier 1 target can safely sit closer to the lower end of the half to 1 month spectrum.

Tier 2: Intermediate Assets (The Yield-Capture Buffer)

- The Strategy: Holding an outsized all-cash reserve imposes a massive opportunity cost. To mitigate this, allocate the next 1 to 2 months of your required reserves into instruments that capture a risk premium over cash while neutralizing interest rate risk and remaining immune to broader stock market crashes.

- US vs. EU Execution: US investors should look to short-term Treasury bills to capture yield. EU investors can utilize short-term government bonds from stable member states (such as German Bunds or French OATs), Euro-denominated short-term bond UCITS ETFs, or fixed-term savings certificates. These assets carry virtually zero default risk but may take a day or two to settle.

Tier 3: Comprehensive Assets (The Income Shock Buffer)

- The Strategy: Income shocks require deep reserves, but because they are much less frequent, these assets do not need to be entirely immune to market risk. You can rely on accessible assets invested for long-term growth, provided you mathematically "overfund" this tier to account for potential market drawdowns.

- The "So What?": If a globally diversified 60/40 portfolio has a historical worst-12-month decline of roughly 32%, a target liquidity of $10,000 requires you to hold at least $14,706 ($10,000 ÷ [1 - 0.32]) to ensure your baseline funds survive a severe bear market. Of course you can always adjust this 32% to higher value.

- US vs. EU Execution:

- US: Utilize taxable brokerage accounts, Health Savings Accounts (HSAs), and Roth IRAs. HSAs act as a highly effective shadow emergency fund; you can reimburse yourself tax-free for qualified medical expenses years after they occur, allowing the assets to compound tax-free in the interim. Roth IRA contributions (though not earnings) can also be withdrawn tax- and penalty-free at any time.

- EU: Investors must look to their specific country's tax-advantaged wrappers. In the UK, utilize an Individual Savings Account (ISA) for tax-free growth and penalty-free withdrawals. In France, leverage a Plan d'Épargne en Actions (PEA) or an Assurance Vie. In Germany, accessible funds might be housed in a standard brokerage account (Depot) utilizing tax-efficient accumulating ETFs.

3. Execution: How to Start and Keep Up the Momentum

Empirical evidence from behavioral finance (Harmenberg, K., & Öberg, E. 2019) highlights that successful saving is driven more by financial behavior and automated systems than by sheer financial knowledge. Here is how to operationalize your blueprint:

- Calculate Your Custom Target: The standard 3-6 month baseline must be adjusted based on your specific human capital risk profile. You require more total liquidity if you are a single earner, have highly variable income (like sales commissions), or possess highly specialized job skills that make finding a replacement role time-consuming.

- Automate and Cascade: Remove the friction of decision-making. Set up automatic transfers from your paycheck to fully fund your safe-and-liquid Tier 1 cash reserve first. Once that quick-asset threshold is met, automatically redirect those cash flows to build your intermediate (Tier 2) and comprehensive (Tier 3) assets.

- Accelerate with "One-Time" Money: Drastically speed up the funding of your buffers by allocating sudden cash infusions - such as a tax rebate, a work bonus, or a financial gift - directly into your emergency tiers.

Practical Example: The Cascading Liquidity Strategy in Action

To see how these steps translate into a real-world scenario, consider an investor named Riley. She earns $60,000 annually with $42,000 in baseline yearly expenses ($3,500 per month).

- Defining the Targets: Riley assesses her job security and determines a total liquidity need of $14,000 (four months of expenses). She decides she needs $2,000 (slightly over half a month's expenses) held in absolute safety to absorb immediate spending shocks (Tier 1).

- Automating Tier 1 (Quick Assets): Starting from zero, Riley breaks her $2,000 cash target into micro-goals. She sets up an automated transfer of $42 a week (roughly $6 a day) from her primary checking to a high-yield savings account. At this automated rate, she fully funds her Tier 1 buffer in under a year without having to actively think about it.

- Cascading to Tiers 2 & 3 (Intermediate & Comprehensive): Once her $2,000 cash buffer is secured, Riley does not simply hoard more cash, which would drag down her portfolio's return. Instead, she cascades her automated $42/week (plus any additional savings capacity) into investments. First, she routes funds to capture her employer's 401(k) match, optimizing her long-term wealth. Simultaneously, she begins funding a Roth IRA.

- The Strategic "So What?": Because contributions to a Roth IRA can be withdrawn tax- and penalty-free at any time, this account acts as her Tier 3 (Comprehensive) buffer. Financial modeling demonstrates that by capping her cash at $2,000 and cascading the rest into accessible market investments like a Roth IRA, Riley achieves a significantly higher median wealth over a 10-year period compared to an investor who insists on hoarding the full $14,000 in uninvested cash before touching the market.

By defining the exact dollar amount needed for immediate shocks and automating the cascade of excess savings into market vehicles, you efficiently build your emergency fund without sacrificing long-term compound growth.

4. Maintenance: Supporting and Managing Your Liquidity

Once your 3-tiered emergency fund is established, it requires systematic management to remain an effective safety net:

- Replenish Immediately After Use: If you experience a financial shock and are forced to draw down your Tier 1 or Tier 2 accounts, prioritize rebuilding that specific bucket immediately so it is available for the next event.

- Monitor Your Human Capital: As you progress through your career, your job security, income variability, and household structure will naturally evolve. Re-evaluate your overall liquidity target annually to ensure it accurately matches your current exposure to income shocks.

- Resist the Urge to Rely on Credit: It is tempting to view a high credit limit as a substitute for liquidity. However, relying on high-interest credit card debt to navigate a crisis severely strains household finances and compounds the initial shock. Maintain your liquid reserves so you are never forced into unfavorable borrowing terms.

Summary: By separating your liquidity needs into a tiered system, you effectively match the accessibility of an asset to the probability of an emergency. This strategy optimizes your household liquidity, protecting your downside risk without suffering the heavy opportunity cost of an oversized cash position.

Strategic References & Further Exploration

1. The Macroeconomic Evidence (The Origin)

- Source: Carroll, C. D. (1992). The Buffer-Stock Theory of Saving: Some Macroeconomic Evidence. Brookings Papers on Economic Activity, 1992(2), 61-156.

- Link: Read the Brookings Paper

- Why it matters to your wealth: This is the foundational study that used household data to prove why treating emergency funds as a dynamic "buffer" against severe income shocks (like unemployment) is vastly superior to standard permanent-income saving models. It established the quantitative rule that your target liquidity ratio must be tied to your specific income uncertainty.

2. The Mathematical Foundation (The Modern Blueprint)

- Source: Carroll, C. D. (2021). Theoretical Foundations of Buffer Stock Saving..

- Link: Read the Theoretical Foundations Paper

- Why it matters to your wealth: This paper updates the 1992 theory, providing the rigorous mathematical proofs for why households engage in "target" saving. For the highly technical investor, this paper also introduces the open-source Econ-ARK toolkit, which allows you to computationally model and simulate your own optimal buffer-stock saving behavior based on these exact economic principles.

3. The Behavioral Execution (The "Wait-and-See" Motive)

- Source: Harmenberg, K., & Öberg, E. (2019). Consumption Dynamics under Time-Varying Unemployment Risk. Working paper, No. 8-2019, Copenhagen Business School (CBS), Department of Economics.

- Link: Read the CBS Working Paper

- Why it matters to your wealth: This research applies the core buffer-stock theory to real-world consumer behavior. It proves that successfully navigating an income shock relies on a two-front strategy: utilizing your 3-tiered liquidity buffers to cover everyday living expenses, while simultaneously leveraging the "real-options" motive to completely halt large, irreversible purchases (like vehicles or home renovations) when your job security is threatened. It demonstrates that financial safety requires spending flexibility just as much as cash reserves.